Understanding the Common Reporting Standards (CRS)

The Common Reporting Standards (CRS) is an international framework established by the Organisation for Economic Co-operation and Development (OECD). Its primary purpose is to facilitate the automatic exchange of financial account information between participating jurisdictions. By doing so, CRS aims to enhance transparency in global tax matters and combat tax evasion. Tax authorities are thus enabled to automatically share information about residents' assets and income, promoting global efforts to prevent tax evasion.

CRS Implementation in Kenya

In Kenya, CRS was introduced through the Finance Act of 2021, which added Section 6B to the Tax Procedures Act (TPA). This section mandates the Cabinet Secretary for the National Treasury to issue regulations for implementing CRS in the country. On February 7, 2023, the CRS regulations were gazetted by Legal Notice No. 8 of 2023, with an effective date of January 1, 2023.

Kenya is also a participant in the Multilateral Competent Authority Agreement (MCAA). On September 9, 2022, Kenya signed the MCAA to exchange country-by-country reports. The MCAA outlines the specifics for exchanging CRS information, including financial account data.

Reporting of Financial Accounts

Under common reporting standards, financial institutions in Kenya are required to report the financial accounts of reportable persons. A reportable person is defined as someone from a reportable jurisdiction, excluding the United States of America and Kenya.

Information Required for Reporting Under CRS

Financial institutions must submit the following information to the Kenya Revenue Authority (KRA):

- An information return on reportable accounts (both pre-existing and new accounts).

- A return marked "nil" if there are no reportable accounts.

Reporting Thresholds in CRS

CRS reporting distinguishes between two types of accounts based on their balances as of December 31:

- Low-value accounts: Accounts with an aggregate balance of less than USD 1,000,000.

- High-value accounts: Accounts with an aggregate balance of USD 1,000,000 or more.

Timeline for Reporting to KRA

Reporting Financial Institutions must file the CRS return with the KRA by May 31 of the year following the reporting year. For 2024, the first year of filing, the deadline is August 31, 2024.

Records Retention

CRS records must be maintained for a minimum of five years after the reporting period.

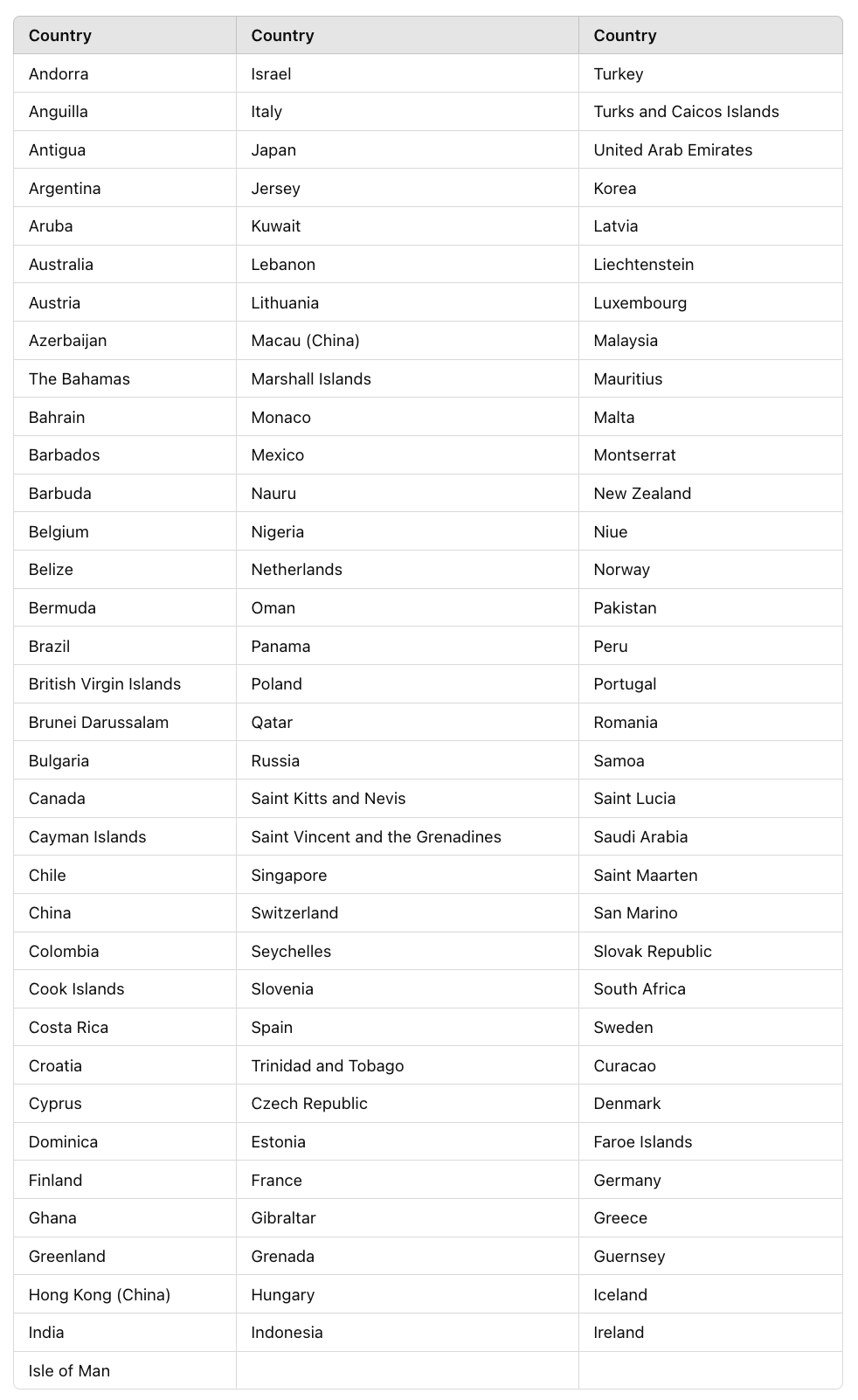

Click here to see the participating countries.

{kind=link}